Part 2 of my full notes and analysis from the past two weeks: September 3-16, 2017. Periodicals covered in this Wall Street Recap include the WSJ, FT, NYT, and LA Times.

The “Burned Cat” Phenomenon

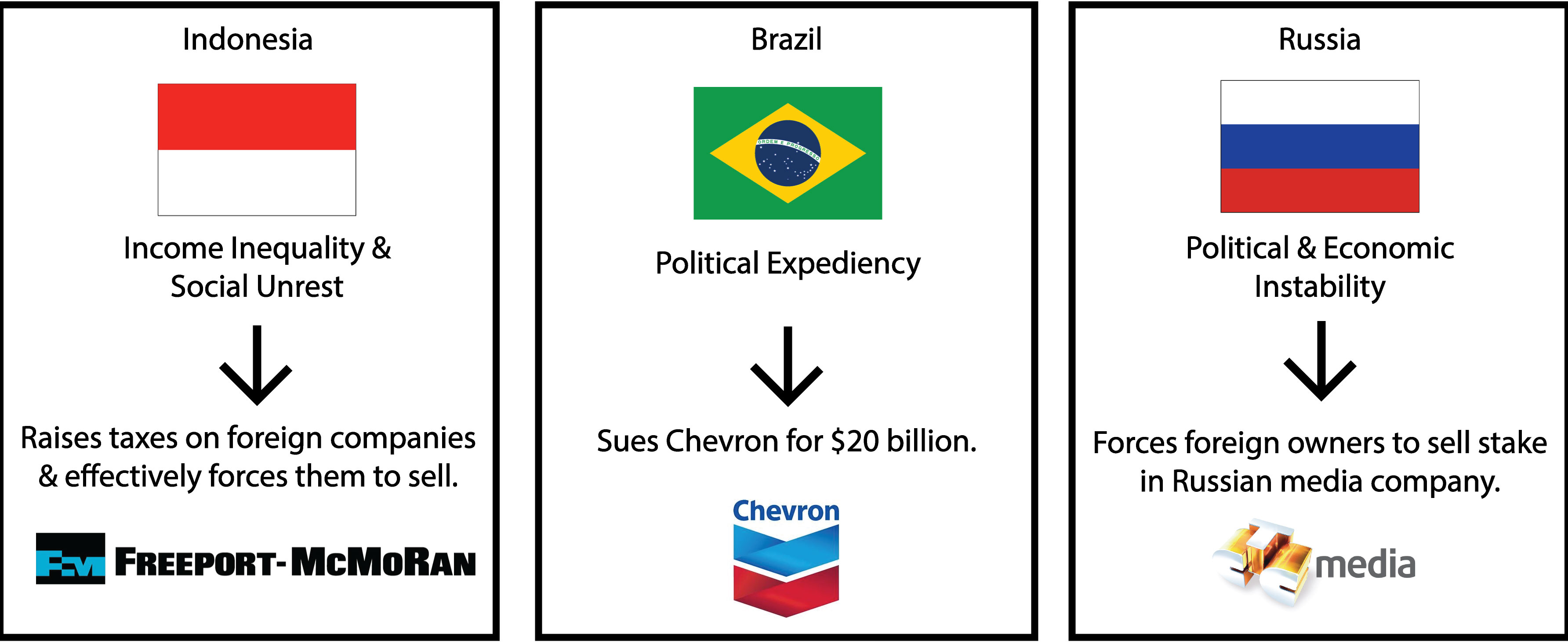

Investors who get burned by an asset bubble often develop a learned apprehension towards that asset class, regardless of its future economics or valuation. In other words, they go about acting like Mark Twain’s cat who, after sitting on a hot stove lid, never sat on a hot or cold stove lid ever again. (link)

Learned apprehension can lead to depressed asset prices as well as severe under-investment in new supply.

1) Depressed asset prices

Investors may develop an irrational resistance towards an asset which has burned them before. Making them reluctant to invest, even at very attractive prices. Example:

Elon Musk

Elon Musk experienced this “Burned Cat” phenomenon while working for a bank early in his career. He found Brazilian debt trading for 25 cents on the dollar, which was guaranteed by the U.S. Treasury for 50 cents on the dollar. He presented this investment idea to the Bank’s CEO who promptly rejected it saying, “the bank had been burned on Brazilian and Argentinean debt before and didn’t want to mess with it again.” (link) Taken aback, Elon tried to explain that you couldn’t lose unless you thought the U.S. Treasury was going to default, making it an effective “no-brainer”. The CEO still declined.

2) Severe under investment in new supply

During an asset bubble, investors eagerly build out new supply, over-extend themselves, and set the ground for their own demise. Following the bust, investors may become hesitant to develop new supply, even when favorable economic tailwinds present themselves. As a result, an industry that was once defined by chronic over-supply, can shift into one defined by chronic under-supply. Examples:

Ethiopian Famine

This feast or famine industry cycle contributed to Ethiopia’s 1983-1985 famine. Having been burned by a bountiful harvest and low prices the year before, “Ethiopian farmers produced less grain and more cash crops or livestock, reducing food production in the following year.” (link)

Ireland Housing

Ireland’s real estate market is experiencing the after-effects of the “Burned Cat” phenomenon. Leading up to the financial crisis, Ireland produced one of the most severe housing bubbles in the world. The subsequent bust resulted in years of under-investment in new housing. The country has since developed a chronic shortage of new homes and property prices are rapidly rising.

As the Financial Times described: (link)

“With Ireland facing a chronic shortage of homes and property prices again rising rapidly,”

“Builders are struggling to meet 10 years of pent-up demand for new homes, while rents are rising and Dublin faces a growing homelessness crisis.”

“Housebuilding, which declined to a trickle after the crash, has stepped up markedly yet acute strains remain. Although private builders are projected to complete 18,000 homes this year, industry figures estimate 30,000 units will be required for years to come.”

“Figures this week showed annual property inflation on a national basis is advancing at 12.3 per cent.”

Misjudgment underpinning the Burned Cat Phenomenon:

“Burned Cat” investments are influenced by a lollapalooza of human misjudgment, including:

- Extra-Vivid Evidence: Investors who have been burned by an investment won’t soon forget.

- Pavlovian Association: Through negative reinforcement, investors learn to reflexively avoid an asset class.

- Over-Influence from Authority: News coverage of a “burned cat” investment is likely to be prominent, negative, and pessimistic.

- Social Proof: No one else is investing in it, so that reinforces the notion that it’s the right thing to do.

- Bias from the non-mathematical nature of the human brain: Investors tend to naively extrapolate past returns which contributes to extreme valuations during bubbles and busts.

Investment Lesson: Actively look for assets that have burned investors. They may present excellent opportunities due to;

- The market’s unwillingness to invest in the asset, even when favorable economics and valuations exist.

- Severe under-investment in new supply, which sets the stage for future supply shortages. (Pay special attention to areas where supply cannot ramp up quickly.)

Standard Causes of Human Misjudgment

Social Proof: Rationalized/Normalized Terrible Behavior

At Home Among the Giants (link)

Wllie McCovey: “I tried working as a bus boy in a whites-only restaurant, but I quit after a week. All the things that make you cringe was normal talk then. You took it or you walked away.”

“The five most dangerous words in business are: ‘Everybody else is doing it’.” – Warren Buffett

Social Proof: Fear of Missing out

Leveraged Loans too Popular (link)

“Some companies that reprice loans have cut debt-to-earnings multiples. But for many, nothing has changed other than the strength of investor demand for debt.“

“When demand is strong, any investor that declines the lower yield risks seeing another buyer take their place, and many are battling to keep their money invested.”

Deprival Super-Reaction Syndrome

That Airline Seat You Paid for Isn’t Yours (link)

“Political commentator Ann Coulter…erupted in a Twitter tirade earlier in July after Delta moved her from a preferred aisle seat to a window seat in the same extra-legroom row.”

“…passengers think they can buy the rights to a specific seat…Airlines say that legally, you don’t.”

Contrast Caused Distortion

Passive Migration: Denver Wins Big as Financial Firms Relocate to Cut Costs (link)

“If you’re talking to someone who’s been in Denver, they’ll say it’s getting unaffordable, but if you’re coming from San Francisco, the reverse sticker-shock is wonderful,” said Ms. Droller.

“And while Denver home prices reached a record in June, they are still far below San Francisco.”

Incentive Caused Bias

Wall Street Needs You to Borrow Against Your Stock (link)

“Morgan Stanley’s finance chief said, ‘that the bank expects more clients to take out loans in the months ahead. ‘That’s been a real key driver of our wealth business.‘”

“The Massachusetts securities watchdog last year accused Morgan Stanley of developing a sales program that encouraged brokers to pitch these loans regardless of whether clients needed them.“

“Several Merrill Lynch brokers said they have asked long-standing clients to open a securities-backed line of credit to help them hit bonus hurdles,”

“The guy tells you what is good for him…So you’re getting your advice in this world from your paid advisor with this huge load of ghastly bias.” – Charlie Munger

Lesson: Watch out for rapidly growing products and services on Wall Street. They likely are associated with massive incentive-caused bias.

Consistency & Commitment Tendency

Wall Street Needs You to Borrow Against Your Stock (link)

Merrill Lynch brokers asked long-standing client to open lines of credit “assuring that clients wouldn’t need to use it or pay any fees for opening it.”

“Brokerage executives have said the longer a client has one of these loans tied to their account, the more likely they are to use it.”

“People think if they have committed to it, it has to be good.” – Charlie Munger

Lesson: Beware of commitments, even seemingly harmless ones.

Lollapalooza Effect: Examples

“I would say the one thing that causes the most trouble is when you combine a bunch of these (causes of misjudgment) together, you get this lollapalooza effect.” – Charlie Munger

LIBOR: Incentive Caused Bias, Pavlovian Association, Social Proof, Envy/Jealousy

The LIBOR was a terribly flawed benchmark. It was easily to manipulate and bankers were highly rewarded for doing so. Everyone around them was doing it, and they were all getting rich. Hence, “studies have estimated that hundreds of trillions of dollars of financial contracts around the world were created based on the benchmark.

Libor: A Eulogy for the World’s Most Important Number (link)

“It turned out that banks were skilled at getting Libor to move in favorable directions. After all, it was their employees who were guesstimating their borrowing costs, so it was simple enough to skew those figures in helpful directions.”

“But government investigations soon showed not only that manipulation was wide-spread and easy to pull off, but also that government officials and central bankers had known for years about Libor’s vulnerabilities but failed to act.”

“If you carry bushel baskets full of money through the ghetto, and made it easy to steal, that would be a considerable human sin, because you’d be causing a lot of bad behavior, and the bad behavior would spread.” – Charlie Munger

Fire Ants in Japan: Stress-Induced Mental Changes, Social Proof, Extra-Vivid Evidence

The sudden stress from the arrival of fire ants in Japan, along with extra-vivid coverage from the media prompted faster and more extreme reactions. Furthermore, Social-Proof amplified the power of this reaction.

Evacuate the Sandbox! Japan Is Freaking Out About Fire Ants (link)

“The mild panic here is partly due to sensationalism in the mass media, with some reports falsely depicting fire ants as murderous,” said Mr. Hashimoto.

“Better safe than sorry, said one wrestler.”

“He drew a parallel in Japan’s experience with how U.S. fire ant infestations in the 1950s were caught up in fear about communism.”

“Shares of pesticide makers have surged on the Tokyo Stock Exchange, and one manufacturer started selling ponchos made from industrial-strength material that allegedly protects the wearer from fire ants.”

“He added, ‘It is necessary for everyone in the nation to recognize correctly the characteristics of fire ants and address the matter calmly.'”

“One consequence of this tendency is that extra vivid evidence, being so memorable and thus more available in cognition, should often consciously be underweighed while less vivid evidence should be overweighed.” – Charlie Munger

{kind=link}