Investing in a foreign country is often akin to investing in non-voting B Shares of common stock or Subordinated Debt. While such investments will allow you to share in a country’s success, it also means that you may share disproportionately in the country’s woes.

Foreign investors are particularly vulnerable to “economic persecution” during periods of political or economic hardship. When a country or political party becomes concerned about self-preservation, foreign investors, who are not part of their “shared identity”, become easy targets for their ire.

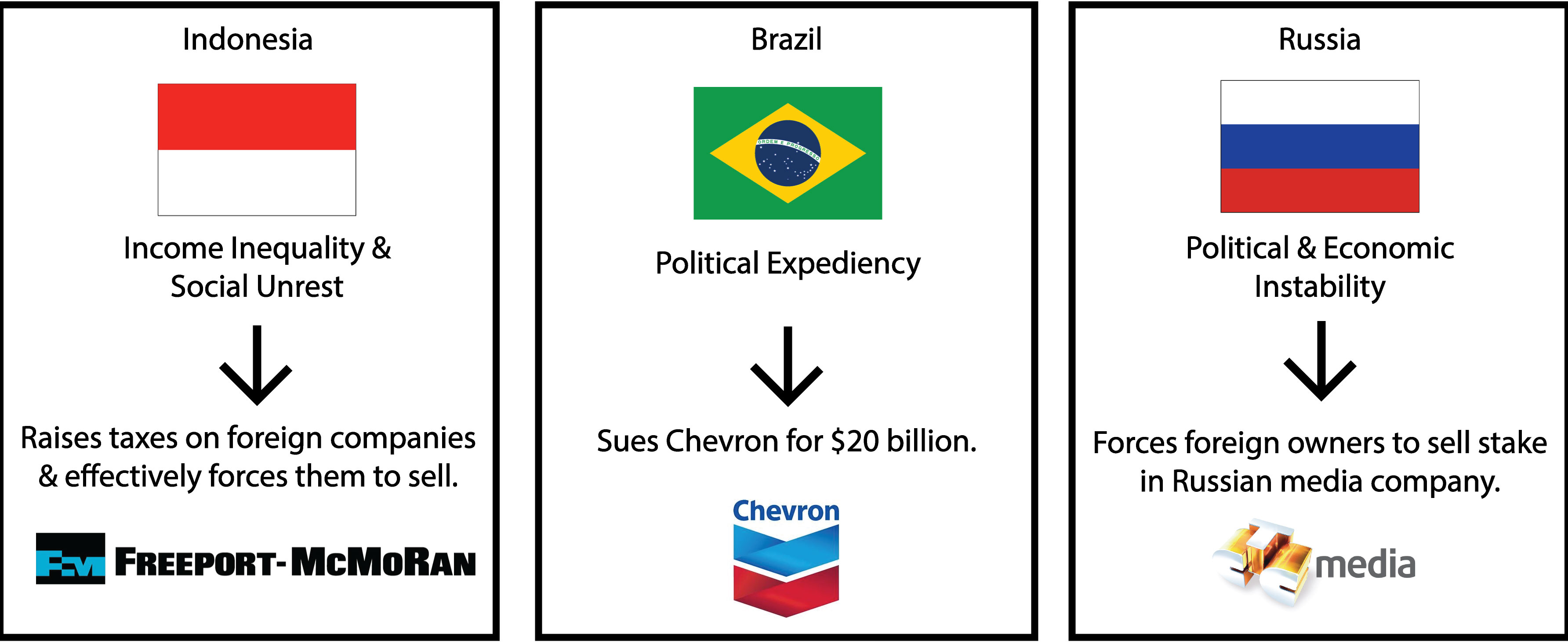

The following are three examples where foreign investors were treated as a subordinated class. From them, we can extract some valuable lessons.

Indonesia: Raise taxes on foreign corporations and ultimately force them to sell.

Indonesia has been targeting foreign copper mining corporations with higher taxes and increased pressure to sell their Indonesian assets to domestic investors.

“As part of its push to earn more from the mining sector, Indonesia banned ore exports and placed restrictions on exports of mineral concentrates in 2014 to push companies to invest in domestic smelting.” (link)

“Indonesia has asserted more control over foreign investment with the aim of redistributing economic benefits in a more equitable manner, an effort that began after the fall of dictator Suharto.”

“It said the divestment obligation was meant to “facilitate” mining companies to join with the government and “bring justice” for the people of Indonesia as the “absolute” owners of the country’s resource wealth.”

“Freeport derives roughly one-third of its copper output from Indonesia.”

Reasons for “Economic Persecution”:

Slowing GDP Growth

“Southeast Asia’s biggest economy has been undershooting the 7 percent growth target set by Widodo when he took office two years ago, mainly due to low commodity prices and weaker global demand.” (link)

Rising Income Inequality

“Inequality in Indonesia is climbing faster than in most of its East Asian neighbors, raising the concerns of many Indonesians,” (link)

“The country’s official poverty rate has halved between 1999 and 2012, falling from 24% to 12%. However, the Gini coefficient, a measure of national consumption inequality, has increased from 0.32 in 1999 to 0.41 in 2012[1]. Hence income distribution has become much more unequal.” (link)

Brazil: Sue the heck out of foreign corporations.

Brazilian prosecutors were surprisingly aggressive towards Chevron after an oil spill in 2011. They sought $20 billion in damages and filed criminal charges against the executives. Meanwhile, State owned oil company Petroleo Brasileiro which owned 30% of Chevron’s well, was not sued by the Brazilian government. (link)

“But Brazil remains a politically challenging place to operate, with complex environmental licensing procedures and requirements that a lot of equipment and labor be made and hired locally.”…”Oil companies were rattled in 2011 when a minor oil spill by Chevron prompted Brazilian prosecutors to seek nearly $20 billion in damages and file criminal charges against executives. The charges were ultimately dropped, and Chevron agreed to pay $42 million to settle the suits in 2013.” (link)

Reasons for “Economic Persecution”:

Politically Expedient: A headline catching $20 billion lawsuit will direct the country’s attention and blame towards Chevron, and away from politicians and regulators. Furthermore, it may help advance political careers or party agendas.

Socially Acceptable: A foreign company is an easy and socially acceptable target.

Russia: Force foreign investors to sell.

In 2015, Russia passed a law limiting foreign ownership of Russian media companies to 20%. There was really only one company affected by this law, CTC Media, whose stock price subsequently crashed. Before the announcement, CTCM had attracted many value investors who were enamored with its strong financials and compelling valuation. (link)

What good is it to own a foreign company if you’re forced to “sell low” every time things get bad in that country?

Reasons for “Economic Persecution”:

Political and Economic Tension: 2014 Russian military intervention in Ukraine, subsequent capital flights, and negative GDP growth due to collapsing oil prices. (link)

The Ruling Political party felt threatened: Foreign ownership in Russian media companies could undermine the ruling political party’s agenda and power, especially during an unstable period.

Tombstones

The financial industry uses “tombstones” to announce particular transactions. Perhaps we should use tombstones to announce economic mistreatment of foreign investors. Using the examples above, I imagine they’d look something like this:

Investment Lessons

Be aware that governments can often turn on foreign companies or investors when it suits them. Before investing in a foreign country, ask yourself:

What percentage of this company’s revenue and profits come from this country?

How critical is this company’s relationship with this country?

Does this company, in any way, undermine the agenda or power of the ruling political party?

Political parties may tolerate minor political subversion when things are stable. But under uncertain political conditions, politicians may act swiftly and harshly against any foreign investors seen as a threat to power.

Is the country’s economy slowing down?

A country with high growth will have less animosity towards foreign investors than one with slowing growth.

Is Income Inequality becoming an issue?

Increasing income inequality creates a hostile political environment for foreign investors. They are the easiest and least controversial of targets.

Are there heightened international tensions with this country?

Does this country have a strong history of protecting foreign investors?

i.e. Does the ruling political party have the autonomy to quickly and effectively subvert the rights of foreign investors?

Whether you’re buying a stock or drafting an NBA player, it pays to avoid standard causes of human misjudgment. (link)

In the case of the 2008 NBA draft, most NBA teams committed a huge error of omission when it came to Russell Westbrook. He went overlooked and underappreciated by nearly everyone but the Seattle SuperSonics. There were three key causes of misjudgment associated with this oversight:

An over-reliance on quantifiable data: Most front-offices calculated too much and thought too little. Russell Westbrook was not a very quantifiable player.

“There wasn’t much data to predict his future. Most experts pegged Westbrook as a mid-first round pick.” (link)

“He didn’t start in high school until his junior season and didn’t earn a scholarship to UCLA until after his senior year. He couldn’t dunk until he was 17 and owes his career to a late growth spurt that shot him to 6-foot-3.”

Anchoring & Adjusting: Anchored to their prior assessments, most front-offices weren’t willing to properly update their old assumptions with new information.

“Westbrook’s combine performance, against players who were supposedly better than him, only made the Sonics more curious. ‘He was the best athlete in the gym,’ Weaver said. ‘I was sitting in my seat trying to contain myself.'”

Social Proof: Most professional basketball analysts and front offices did not list Russell Westbrook near the top of their draft lists. Those relying on social proof likely assumed that the crowd’s consensus was rational and accepted it as accurate. Ed Thorp calls this behavior ” the lunacy of lemmings”. (link)

“One day, Weaver went to Presti’s office and declared: ‘I’m looking at everybody, and I don’t understand why this guy is not the best of the group.'”

Investment Lessons:

Standard Causes of Human Misjudgment create great investment opportunities…just so long as you can avoid them yourself and remain objective. In essence, follow the advice from the poem “If” by Rudyard Kipling;

“If you can keep your head when all about you are losing theirs…” (link)

Not everything can be quantified. As Charlie Munger says;

“There’s never going to be a formula that will make you rich just by going through some numerical process. If that were true, every mathematical nerd that gets A’s in algebra would be rich. That’s not the way it works.” (link)

Qualitative Investments can be very lucrative. Warren Buffett’s best investments have been qualitative in nature;

“Interestingly enough, although I consider myself to be primarily in the quantitative school…the really sensational ideas I have had over the years have been heavily weighted toward the qualitative side where I have had a “high-probability insight”. This is what causes the cash register to really sing.” (link)

The Seattle SuperSonics relied on qualitative factors such as Russell Westbrook’s character, competitive drive, and shear athleticism, to develop a high-probability insight that paid off in spades. (link)

“That was the day Westbrook sold him. Presti and Weaver looked athis story-overcoming the odds to become an indispensable part of a winning team-and saw his relentless competitive streak. ‘We don’t know how good Russell Westbrook will be,’ Presti said, ‘but the person that Russell Westbrook is will allow him to maximize his potential.'”

My full notes and analysis on the Wall Street Journal from the past week: February 20-26, 2017 (Week 8). Please Enjoy.

Donald Trump: Pre-Suasion genius?

Is Donald Trump a Pre-Suasion genius? He is constantly criticized for being too vague about the details of his plans and chronically leaving people in a state of uncertainty. But that might just be the key to his success.

Stock markets typically reject uncertainty as a negative force. But in the case of President Trump, markets have embraced a sort of “positive uncertainty”. In his book Pre-Suasion, Robert Cialdini provides a compelling insight which may explain Trump’s strong positive influence on the stock market:

“During the experiment, the men who kept popping up in the women’s minds were those whose ratings hadn’t been revealed, confirming the researchers’ view that when an important outcome is unknown to people, “they can hardly think of anything else.” And because we know, regular attention to something makes it seem more worthy of attention, the women’s repeated refocusing on (the guys whose ratings remained unknown to the women) made them appear the most attractive.” – Robert Cialdini

Now let’s look at an excerpt from an article the other week titled “Federal Reserves Eye Aggressive Rate Increases.” (link)

“President Donald Trump’s plans for tax cuts, new spending and deregulation have buoyed market hopes of faster economic growth and higher corporate profits. But Fed officials at the meeting underscored their uncertainty about the details and effects of the potential policy changes, according to the minutes.”

“A few policy makers also worried that investors betting on tax cuts “which might not materialize” had pushed up equity prices too much.”

Copper prices surged more than 30% in the last year and shares in Glencore have more than tripled in the past 12 months. The two biggest drivers in copper prices over this time-period were:

1) China Stimulus: “The metal’s resurgence partially has been driven by a government economic stimulus program in China, where over 40% of the world’s copper is consumed.”

2) Labor Disputes: There have also been “snags at two of the world’s largest copper mines-labor problems at Chile’s Minera Escondida, and a permit dispute with the Indonesian government for Freeport-McMorRan Inc.’s Grasberg mine.”

So I’m curious…how many investors in Glencore identified “China Stimulus” and “Labor Disputes” as the main parts of their investment thesis? My guess is very few.

“Histogram Management”

Charlie Munger once mused about The Kellogg Company that there’s nothing keeping cereal producers from going crazy over market share and tearing each other apart. (link) So when investing in an industry, you have to seriously consider; What force is maintaining rational economic decision-making in this industry?

The CEO of Glencore appeared to be surprised and upset when his competitors weren’t acting rational in the wake of declining commodity prices.

“(Glencore) CEO has long criticized his competitors for ramping up supply in the face of falling prices.” (link)

Such a reaction seems to indicate a lack of understanding of human psychology and the forces that drive rational economic behavior. After all, there are many reasons management would ramp up production in the face of declining prices. Here are four such reasons:

1) Incentive-caused biases linked to executive compensation or job security.

2) Prisoner’s dilemma and the Fear of Missing Out. Which explains why two rational individuals might not cooperate, even when doing so is in their best interest.

3) Social Proof. You look around and no one is cutting production, so this must be the right thing to do.

4) A genuine economic desire to survive. i.e. They keep producing at a loss in order to cover massive fixed costs.

Expanding upon the first point of Incentive-caused bias, management may have a personal economic incentive to manage earnings based on compensation packages. I like to think of this behavior as “Histogram Management.”

When commodity prices are declining, the easiest way for a mining company to show stable and growing profits is to rapidly increase sales in the wake of declining margins. This strategy of channel stuffing may provide stable earnings figures in the short-term, but it will exacerbate the problem for the entire industry over the long-term.

(Image via Latticework Investing)

Investment lessons:

1) Management often won’t behave in economically rational ways. Therefore, watch out for industries which allow for competition to intensify to the point of mutually ensured destruction.

2) Poorly designed executive compensation can make or break a company/industry.

In other words, don’t give them the rope with which to hang you.

Car Sales Eating into Macy’s Business?

Macy’s CEO said that record U.S. car sales indicate consumers have spent a bigger portion of their budget on bit-ticket items lately.

“At some point in time you’ve got to believe that everybody’s going to have a brand-new car,”…”There’s dollars that are going to be freed up for other categories of spending.” (link)

It makes sense too. Car purchases are highly interest rate sensitive. A majority of new cars are purchased with debt. Today the APR on an auto-loan starts at 3.12%. Meanwhile the APR on a Macy’s credit card is 24.5%. It’s no wonder that sales of goods that can be bought with debt have done well, while cash-based retailers have struggled.

1) Home sales booming on historically low inventory (link)

January home sales reach highest level since February 2007, on the back of the lowest inventory levels on record (circa 1999).

“Home sales rose in January to the highest level since February 2007, a sign that last year’s momentum extended into 2017 despite a limited supply of properties for sale and rising prices.”

“Inventory rose 2.4% at the end of January from the end of December, when supply hit the lowest level since the Realtors association began tracking all types of supply in 1999.

Apartment supplies are growing rapidly, as a result, loans are getting more expensive and harder to come by, and rent growth is slowing.

“Swelling supplies of apartment units are prompting big banks to pull back from new projects, forcing developers to scramble for capital.”

“I haven’t seen anything this seismically different since 2008, when credit dried up.”

“fresh supply is beginning to overwhelm demand.More than 378,000 new apartments are expected to be completed in 2017, a 30-year high,”

“Commercial mortgage brokers said they are seeing and uptick in mezzanine loans…(and) a rise in preferred equity, which also come with higher payments than bank loans…”

“Other developers are turning to smaller regional banks, such as Bank of the Ozarks, which can command higher rates,”

All around the world, corporate debt has proved a popular investment class so far this year…

Asia: “Nowhere is the trend more surprising than in Asia, where money has kept flowing into even the riskiest debt. The extra yield, or spread, investors demand for holding both investment-grade and high-yield Asian corporate debt versus risk-free U.S. Treasuries has narrowed since the U.S. election last November and is heading towards its tightest levels since 2008,”

U.S.: “U.S. corporate-bond spreads are at their tightest in two years.”

Europe: “In Europe, investors also have continued to pile into corporate credit in countries like Germany and France, despite uncertainty created by key elections…”

Areas where I see potential problems with corporate debt demand:

1) Naive Extrapolation of past default rates in Asia: “The default rate on high-yield corporate bonds was lower in Asia than in the U.S. last year at 1% versus 3.6%.”

2) “Risk on”: The voracious search for higher yields: “With interest rates globally still low by historical standards, cash-rich investors are on the lookout for higher-yielding assets. Total household wealth is growing more rapidly in Asia than elsewhere globally, up 4.5% in 2016 to $80 trillion,”

4) China developments

Two fascinating highlights on China:

1) “Of the more than 11,000 public-private partnerships that China has announced since 2014-inwhich companies finance, build and manage commercially viable state ventures-88% remain in preliminary stages and none are complete,” (link)

2) “Since coming to power in late 2012, Mr Xi has eroded the consensus-driven, collective-leadership model of his recent predecessors, taking personal charge of the military, the economy and most other levers of power.” (link)

5) Equity Markets

Two fascinating highlights on China:

1) “The declines paused a rally that has sent the index to 19 fresh highs in 2017-its most records in a year since 1999,” (link)

2) “Companies in the S&P 500 traded at about 22 times their past 12 months of earnings as of Wednesday, above their 10-year average of 15.8,”

3) “The S&P 500 has a forward price/earnings ratio of 17.6, the highest multiple since 2004 and above the averages of the past five, 10, 15 and 20 years.“(link)

Organic Farming: The high labor cost problem

U.S. farmers are quite good at conventional farming where emphasis is placed on efficiency. But consumer demand has been shifting towards organic food, which is less efficient to farm, and requires higher labor costs.

Naturally countries with cheap labor will have a competitive advantage on the U.S. Consequently, U.S. farmers have been feeling the pressure from international organic farmers.

“Organic grain is flooding into the U.S., depressing prices and drawing complaints from domestic organic farmers…” (link)

Specifically, the article talks about pressure from Turkish farmers.

“Turkey vaulted ahead to become by far the biggest supplier of organic corn and soybeans to the U.S. last year…(they) shipped to the U.S. 400,000 metric tons of organic corn, nearly quadrupling its prior-year total, while soybean shipments climbed by more than eight times,”

It’s beneficial to dwell on Turkey for a moment because Turkish farming data helps highlight the competitive challenges that U.S. organic farmers face. Firstly, Turkey’s minimum wage is $6,000/year giving them a competitive advantage in labor-intensive crop production. Secondly, the barriers to entry into organic farming are nearly non-existent. From 2002 to 2014 Turkey’s Organic Farming area increased at an annual growth rate of 22.56%.

And from 2005 to 2012, organic production went from 421,934 tons to 1,750,127 tons. (link)

It would seem that the shift to organic farming is akin to switching from industrial production lines to hand craftsmanship. The countries with the cheapest labor would naturally have the upper hand.

Note: Additional factors which have added to the pain for U.S. organic farmers include a strong U.S. dollar, and accusations that international organic farmers face weaker regulatory oversight.

Activist Defense Strategy?

Management can sometimes react poorly to unwanted activist investors, leading them to make poor economic/ethical decisions. The following case got me thinking about the possibility that management may revert to unscrupulous methods to increase revenue at a poorly performing unit in order to save it from activist pressures.

ABB Hit by Fraud in South Korea (lInk): “The disclosure (of stolen funds) adds to the pressure on CEO Ulrich Spiesshofer as he tries to fend off Swedish activist shareholder Cevian Capital. ABB in recent weeks announced a string of large orders at its power-grid unit, including a $640 million project to deliver an electricity-transmission link in India, but Cevian has been urging ABB to sell the unit.

From the management’s perspective, it would be easier to defeat activist shareholders if the under-performing unit started “out-performing”. Incentives of this kind may increase the likelihood of unethical revenue enhancement tactics like

Channel stuffing or

Signing sweetheart contracts that are overly generous to clients.

Both of these tactics would make the unit appear more successful just long enough to win over shareholder support and stave off activist shareholders.

I’m not saying that ABB is doing this, but from a standpoint of “incentive-caused bias”, it’s more apt to happen. I’d like to see a study on this topic.

Don’t try to “out-Bezos Bezos”

“We’re not going to out-Bezos Bezos,” Buffett said, in response to a question about the effect of online retail on traditional retailers.

It feels like a lot of retailers are trying to out-Bezos Bezos these days.

Wal-Mart: “The retail behemoth is investing billions to raise U.S. store worker wages, lower prices and expand e-commerce sales to better compete with Amazon.com Inc.” (link)

Target: “Target’s CEO vowed to invest billions of dollars to lower prices and remodel hundreds of stores, an admission that the retailer’s focus on trendy merchandise wasn’t enough to attract shoppers.” (link)

Charlie Munger: Slime Pricing Theory

Great example of pricing theory under pavlovian association and information inefficiencies.

Knead Slime? These Business Girls Can Fix you Up (link)

“Just now, she is puzzling over price theory. She asks 50 cents an ounce-a generous handful-but some friends charge more than twice that. ‘They’re getting more sales and I’m not sure why,’ says the seventh-grader in Issaquah, Wash. ‘My slime is the same quality'”

Charlie Munger: Bias from pavlovian association

“In many cases when you raise the price of the alternative products, it’ll get a larger market share than it would when you make it lower than your competitor’s product. That’s because the bell, a Pavlovian bell — I mean ordinarily there’s a correlation between price and value — then you have an information inefficiency. And so when you raise the price, the sales go up relative to your competitor. That happens again and again and again. It’s a pure Pavlovian phenomenon.” (link)

Social Change becomes Economically Viable

Corporations are rarely agents for social change…even if they pretend like they are. Rather they’re economic agents who weigh supply and demand issues carefully. Demand for a socially beneficial product or service usually needs to hit critical mass (aka “The Tipping Point“) before companies “make that change“. Here are some social changes which have reached critical mass and have become economically viable.

Charlie Munger: The prognosticator of Brazilian graft

I read this article on Brazilian graft and I couldn’t help but be reminded of a talk Charlie Munger gave back in 2003. The scenario he gave for bribing a purchasing agent is almost identical to the problems which were uncovered in Brazil 12 years later.

Charlie Munger:

“Now tell me several instances when, if you want the physical volume to go up, the correct answer is to increase the price?…Suppose you raise that price, and use the extra money to bribe the other guy’s purchasing agent?” (link)

Now here’s what happened in Brazil…

“As part of Operation Car Wash, Brazilian prosecutors have accused executives from Petrobras, the state-run oil company, and some of the nation’s largest construction firms of colluding for more than a decade to inflate the price of contracts, kicking back a portion of the ill-gotten gains to lawmakers and other political officials.”(link)

Caution: A.I. will be programmed to exploit your psychological biases

Watch out for a future where Artificial Intelligence is programmed to exploit your psychological biases better than any human can. Charlie Munger warns heavily about this kind of psychology manipulation:

“Now if the human mind, on a subconscious level, can be manipulated that way and you don’t know it, I always use the phrase, “You’re like a one-legged man in an ass-kicking contest.” I mean you are really giving a lot of quarter to the external world that you can’t afford to give.” (link)

It has already started on a small scale:

“Stanford University found a male computerized voice was perceived to be a better teacher of computers, while a female one was preferred for guidance on love and relationships.” (link)

“There’s also the potential subconscious influence. Are we more likely to buy Alexa’s Valentine’s Day gift suggestions if they’re delivered by a female voice? Will a male voice convince us to spring for an expensive leaf blower?”

“73% of teens have access to a smartphone…Those teens are checking their phones on average more than 80 times a day,”

“Packed schedules, helicopter parenting, and the decline of walkable neighborhoods…The net effect is that teens are spending more time indoors, and les active, than ever.”

“Young people today are sedentary for more than 10 hours a day,”

“Gracie says she’ll turn off the TV and talk to friends if they turn up on Houseparty ‘because that’s just better.’

“who wouldn’t want to be able to check in with their best friends whenever they felt like it?

Quote of the week:

“There were no negative tweets, so that’s a good sign.” – Portfolio Manager in response to Bayer’s CEO meeting with Mr. Trump. (link)

Could the best investment quote of all time come from Napoleon? Quite possibly. It was in the unlikely place of Napoleon Bonaparte’s personal diary that I found one of the best investment passages I’ve read. Bursting with investing wisdom, it would be understandable to mistake Napoleon for Warren Buffett. Although he’s writing about the art of war, the insights apply to investing just as well.

Interpretation

Below I dissect Napoleon’s journal entry to ascertain its valuable investing insights.

Importance of mathematics & probabilities:

To be a good general a man must know mathematics; it is of daily help in straightening one’s ideas. Perhaps I owe my success to my mathematical conceptions

Beware of forecasts. Buffett & Munger don’t invest in a company if they can’t see its strength displayed through history:

a general must never imagine things, that is the most fatal of all.

Eliminate psychological biases & crude heuristics which skew one’s perception of reality:

My great talent, the thing that marks me most, is that I see things clearly;

Identify the main issues and ask the right questions:

it is the same with my eloquence, for I can distinguish what is essential in a question from every angle.

Practice Bayesian updating:

The great art in battle is to change the line of operations during the course of the engagement; that is an idea of my own, and quite new.

Keep it simple. Stick to the fundamentals and common sense:

The art of war does not require complicated maneuvers; the simplest are the best and common sense is fundamental. From which one might wonder how it is generals make blunders; it is because they try to be clever. The most difficult thing is to guess the enemy’s plan, to sift the truth from all the reports that come in. The rest merely requires common sense;

Stay curious. Do a lot of reading & research lots of companies. Eventually you’ll come across a good idea:

it’s like a boxing match, the more you punch the better it is.

{kind=link}

{kind=link}